Reinventing My Former Investing Self

Undoing years of aimless investing.

Courtesy: Worthpoint, 1973 Cooper Hockey Equipment Catalogue

When I was 10 years old, my father bought me 10 shares of Cooper, the sporting goods company, and that sparked my first interest in investing.

I’m sure my dad, who was the president of his father’s stock brokerage firm, Alfred Bunting & Company, figured Cooper was a natural choice to get me interested in investing because I played hockey, loved Dave Keon and the Toronto Maple Leafs, and enjoyed following the statistics of the National Hockey League.

My First Stock

My father taught me how to read the stock tables in The Globe & Mail newspaper. I would check Cooper’s price every day. I would love to tell you at this point that Cooper shares provided a big profit and sent me on my way to future investing success. Or that the stock went to zero, and I learned an important lesson about money and risk.

I lost track of my Cooper investment. My memory is hazy why. I may have had the physical share certificate, but I don’t recall. Cursory research shows that Canstar Sports bought Cooper, the parent company of Bauer Hockey, and Nike acquired Canstar Sports in 1995. As a result, they phased out the Cooper name, and my investment died of neglect. That would not be the first time I wasted my dad’s money.

Next Stock, Same Result

When I was a teenager, I must have saved up money because I asked my father what a good investment might be. He sent me to a colleague of his who suggested New Gateway Oil & Gas. I bought $400 of that stock, as I remember. That investment met the same fate as my Cooper shares.

I’m sure you’re sensing a pattern. So am I, as I remember these careless misadventures. But as comedian Brian Posehn said, when telling a story in a standup special about a woman he was undressing for who was aghast at what she was seeing, “Oh, it gets worse.”

Image: Sactown

Comedian, actor, writer Brian Posehn

“What’s There to Think About?”

Maybe not worse but definitely not much better. My former self continued to follow the investment world from a distance, lacking the resources I considered necessary to get involved.

It wasn’t until my early thirties that I called the CEO of a well-known Canadian mutual fund company that I had interviewed to request he refer me to one of his employees to recommend some funds.

I met with this person in his office who, in a soothing voice, explained and then recommended four of their funds. I said, “I’ll think about it.” His pleasant demeanor disappeared, and he blurted out, “What’s there to think about?”

I felt pressured because he showed annoyance at having to meet with me, and now my hesitation put him at risk of not closing the sale. As a general avoider of conflict, I agreed to invest in the four funds he recommended. Happily, those funds performed well for several years until, in need of cash for a move to a different city, I sold all of them.

Imperfect Timing

My next foray into investing was in 2000, during the technology boom.

My father had gifted me and my two older sisters money to limit inheritance tax. I asked him in a phone call whether he thought I should invest in stocks.

By now, my dad was president of the Toronto Stock Exchange (TSE). One would assume he would have a bias towards purchasing shares in various corporations, or mutual funds or ETFs, the latter of which he and his team had pioneered at the TSE.

But my dad said something to the effect of,

“If you believe certain companies can do well in the long term and that the market will keep going up, then you should invest in the stock market.”

He left my decision up to me or didn’t want to be responsible for or want to know about what I did with the money, which was fair and generous.

After paying down some debt, I put half of the money into four mutual funds and the rest into select technology stocks, such as Nortel Networks and Research in Motion.

The day I bought those stocks in March 2000 was the same day the Nasdaq Composite had a wild, intra-day swing plunging several hundred points only to climb back and finish flat on the trading session. I was at a friend’s place. We were glued to CNBC throughout the afternoon. It was the first major prick in the technology bubble, which burst in the fall of that year.

My tech stock investments cratered, and I redeemed my mutual funds to help finance my girlfriend and me in raising our two-year-old daughter. I was not the only one who saw the tech crash vaporize their investments and teach them a massive lesson about manias and bubbles. Unperturbed, I moved forward.

From Sports to Business

Career-wise, before the dot-com crash, I left The Sports Network after 12 years when they did not renew my contract and started looking for a new gig, which I soon realized was on business television as I watched (got caught up in) CNBC’s coverage of the raging bull market (bubble) in tech stocks.

My skills were transferable and my goal became to get an on-air job at Report on Business Television (now BNN Bloomberg), a cable channel that started broadcasting in 1999.

After stints reporting on sports and then business at CFRB Radio in Toronto, and at a weekly, national business television show, I achieved that goal, which propelled me to a 15-year run at BNN as a reporter and anchor.

I then became much more immersed in reading and doing research on investing and business, learned a lot, and interacted with and interviewed people I perceived to be smart, educated, and successful portfolio managers.

During that time, I took part in the defined contribution retirement plan of BCE, BNN’s owner, whereby I regularly contributed a chunk of my salary to the plan and they matched it. When I left BNN, I transferred that account to my wife, a professional money manager, for her to manage.

My Hedgeye Revelation

Despite this education in investing, I still had no proper plan for my personal account beyond taking risks and trying to hit home runs with my attention bouncing between the latest shiny things such as gold, silver, certain small caps and cannabis stocks.

It wasn’t until I discovered Hedgeye Risk Management and Keith McCullough’s global macro, full investing cycle, data-driven process that I realized there was a viable and far superior alternative to my indiscriminate way of investing, and to traditional buy-and-hold, long-term investment strategies.

Many have achieved success by constructing a diversified portfolio of shares of exceptional companies, holding onto them for extended periods, and outperforming the market. After all, I trust my wife to do just that.

But, as an alternative for my personal account, other DIY investors and institutions, the Hedgeye investing process is deep, rules-based, and considers “the flows of the machine” (the underlying machinations of the market), which now often overwhelm traditional fundamental metrics used by portfolio managers to assess a company’s prospects.

Tier1 Alpha

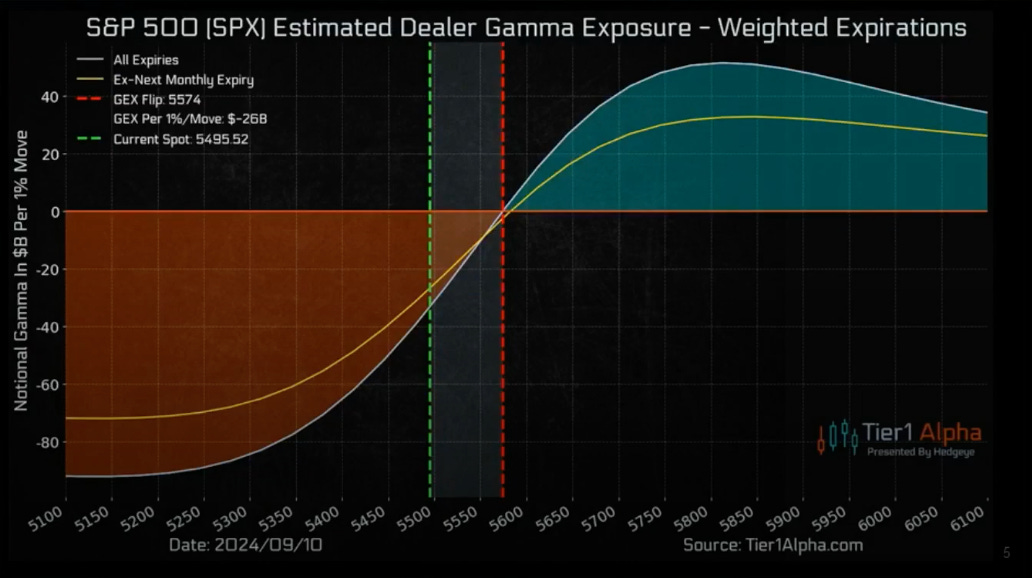

Hedgeye partner Tier1 Alpha tracks the systematic positioning of multi-billion dollar Volatility Control Funds, Commodity Trading Advisor funds, and Risk Parity strategies.

These funds are programmed to buy or sell strictly based on options dealer gamma* and the “flip line” level at which the S&P 500 moves from positive to negative gamma or visa versa.

Having only a basic understanding of options, it’s an aspect of the market I’m still attempting to fully grasp.

Hedgeye is helping to educate me and other investors by presenting a Real Conversation this past week with McCullough and the heads of Tier1 Alpha. This is well worth your time to better understand the influence of the plumbing within the markets that the mainstream financial media rarely talks about.

Watch it here: A Masterclass on Modern Market Structure: Inside Options, Flows & Volatility

(*For any Hedgeye process questions, check out their resources at Hedgeye University.)

Tier 1 Alpha chart (from September 10) showing negative Dealer Gamma Exposure (the lines representing S&P 500 options intersecting the green dotted line), which can lead to increased market volatility. Positive Dealer Gamma Exposure can lead to lower market volatility.

A price-to-earnings ratio (P/E), for example, has its place in assessing a stock, but it’s just one factor and, as McCullough has said, valuation is not a catalyst. Rates of change in revenue, EBITDA, and free cash flow (the pods) are catalysts.

A P/E ratio is far less relevant to the movement of a stock than a multi-billion-dollar volatility control fund programmed to buy or sell vast swaths of stocks based on the aforementioned metrics.

My aim now is to shed every layer of my former investing self who, as I’ve detailed, was unfocused and scattershot. This former self is fading into the past but is still hanging on and sometimes imposes himself on my decision-making just to screw with me.

But by continuing to refine my use of the Hedgeye process with discipline and proper execution, one day I’ll be able to say goodbye to my old investing self.

Next Saturday: If You Don’t Want to Play That Way, Don’t Play That Way

Disclaimer: I do not have any financial arrangement with Hedgeye. I do not intend for this series to be construed as investment advice, instructional nor promotional. Dan Holland, Hedgeye’s Head of Media and Public Relations, has been gracious in making my writing available on Hedgeye’s website.

Thank you.

Interesting read! Keep it up.